Here are the big takeaways from the NIC data release.

By Steve Moran

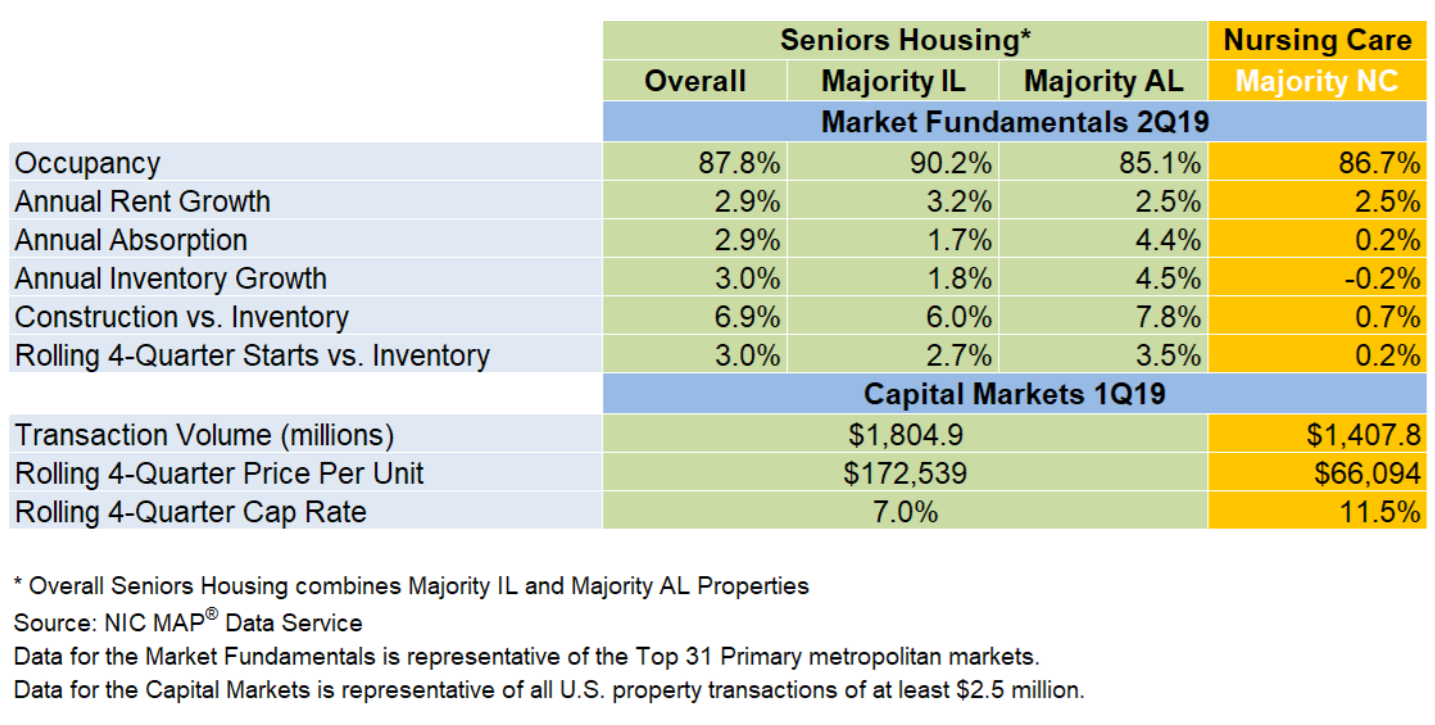

NIC just released their Q2 2019 data report. Here is what it looks like in Charts and Graphs:

Here are the big takeaways from the NIC data release:

-

Everything is down a bit.

-

Overall occupancy in Q2 hit 87.8% down from 87.9% a year ago and the lowest level since 2011.

-

The two best markets were San Jose, CA, at 95.7% and Portland, OR, at 91.6%.

-

The worst markets are Las Vegas, NV, at 82.3% and Houston, TX, at 81.1%.

-

A year ago San Antonio, TX, was at 78.5% and is now at 82.9%.

-

There is a clear slowdown in construction starts, which is working through the pipeline. In some cases those slowdowns are really significant.

-

Assisted living is doing less well than independent living, coming in at 85.1%.

-

New construction starts in the 31 primary markets total 19,113 for the last four quarters.

Does It Mean Anything?

I spent a bit of time chatting with NIC’s chief economist Beth Mace as she was catching a flight about the findings but because we were both in a rushed situation, I will own all of these observations, not wanting to unfairly attribute my thinking to her. Except if you find something you think is super brilliant, give Beth all the credit:

-

These are national averages and, as such, don’t tell you much about the individual markets as some of the above bullets confirm.

-

While we seem to still be bumping along at a place where more new supply is entering the marketplace than is needed, it is not a huge imbalance and there is strong evidence the pipeline is slowing way down.

-

Because we are so close to even and markets are really spiky from quarter to quarter, things can change significantly, like San Antonio.

-

The economy seems to continue to be in a stable growth mode that seems likely to continue through the end of the year and could very well continue up to the election.

-

I see two areas of concern. The debt continues to grow at a rapid rate. It puts our kids and grandkids at serious risk with no one in power seeming to have any real interest in dealing with it, even though most acknowledge it as a problem.

-

It seems as if we are in a situation where the downside risk is much higher than the upside opportunity. What I mean by this is that even if the economy became much more robust it is unlikely we would see a huge increase in demand or rate.

On the other hand, if the market has even a modest softening, it could have a really big negative impact on existing pipeline inventory.

-

There does not seem to be any movement in market penetration.

What It Really Means

I continue to believe that, as an industry, we are mostly falling short in broadening our appeal to consumers. If we had a bigger variety of offerings, both programmatically and from a price point, we would attract more residents. The most critical thing we need to be focused on is making aging and senior living look cool. You may think it is impossible, but I think Chip Conley with his Modern Elder Academy is proving that it is possible.

I remain convinced that Chip could be, should be, our guiding light in transforming the coolness of aging.

Finally, do a deeper dive with Beth and the NIC team about market conditions at the NIC Fall Conference. We will be there and would love to connect, maybe do an interview?